Sep 27 | 2019

Underlying Strength but Disruptors Still Wild Card

Dynamar B.V.’s biennial study on the breakbulk industry is an in-depth analysis of breakbulk, heavy-lift and project vessel operators and services. In conversation with Carly Fields, Dirk Visser, author and managing editor for Dynamar, reveals exclusive content from its 2019 edition of the report, Breakbulk V – Operators, Fleets, Markets.

Q: What were you particularly surprised by in this edition of your report?

A: Companies come and go, get bigger or shrink, but of definite amazement is the fast emergence and growth of Zeaborn. Dynamar’s previous breakbulk report from mid-2016 noted that the company had ordered 12 multipurpose/project/heavy-lift ships – which were subsequently rejected – but that it was not yet actively operating.

Nowadays, it incorporates the major brands of Rickmers Line with its semi-liner services, Zeamarine with its tramp services, the commercial management of part of the Carisbrooke (UK) fleet and the chartering activities of the HC Group, MCC Marine and NPC Projects, among others. In addition, the company is active in ship management and ship owning. And it’s not finished yet. Zeamarine had stated a goal of operating some 100 multipurpose ships by early 2019, although as we leave the third quarter that goal has not yet been achieved.

Q: I note that you comment in the report on the rising star of vehicle carriers and that they are making their presence increasingly felt in the breakbulk sector. How do you see this trend developing over the coming years?

A: In the report, we refer to the operators of vehicle carriers, container ships, reefer vessels and dry bulk carriers as ‘disruptors’ as, apart from their core business, they also carry breakbulk – the bread and butter of traditional breakbulk operators. Of those four disruptors, vehicle carrier operators have developed into formidable breakbulk operators.

For most vehicle carrier operators, non-carloads account for up to 30 percent of total liftings and in some isolated cases as much as 40 percent to 50 percent of their total liftings. On the delivery of the first in a series of six 8,500 car-equivalent-unit, post-Panamax car carriers – which are still the world’s largest – Höegh Autoliners said: “With these ships we target the breakbulk market.”

Typical cargoes moving by car carriers include boats and yachts, high-and-heavy, machinery and tools, mining equipment, power generation plant, railway coaches and locomotives. There are also pallets and big bags, all mobilized on cassettes, MAFIs, chassis and other rolling equipment. It is now a fact: the vehicle carrier is a formidable breakbulk vessel.

Q: With that in mind, are you concerned about the proportionately larger orderbook for roll-on, roll-off ships?

A: Not really. After all, car carriers are primarily built to carry cars which, under normal circumstances, is big business. However, we see the conventional ro-ro ship ultimately being replaced by a car carrier-like vessel. For example: Wallenius Wilhelmsen Ocean has earmarked eight of its ships as ro-ros rather than a car carriers. The difference? A missing side ramp, a heavier quarter ramp and strengthened and higher project holds, with some able to sustain loads of up to 10 tons per square meter. Some of these ships can also take cargo on deck.

The number of conventional deep-sea ro-ro operators has come down substantially. There is now Grimaldi, WWO, NYK Bulk and Project Carriers, Messina Line and Bahri; that’s about it.

Q: What changes of note have there been in the Top 25 fleet ranking for this edition?

A: Staying with the Top 25 combined breakbulk/roll-on, roll-off carriers – the multipurpose operators – there have been quite a number of changes, in part reflecting the consolidation taking place in the industry.

Examples are the two major forest product carriers with their mighty open-hatch cargo ships: G2 Ocean – the October 2017-formed joint venture between Gearbulk and Grieg Star – and Saga-Welco – formed in 2014, and ultimately owned by NYK and Westfal-Larsen.

In May 2018, Intermarine of the U.S. and Zeaborn from Germany formed the joint 25:75 venture Zeamarine. Barely a year later, Zeamarine became a fully owned subsidiary of Zeaborn, which also owns February 2017-acquired Rickmers Line.

Also in 2017 but toward the end of year, Hamburg-based multipurpose liner operator MACS, serving Southern Africa, acquired Hugo Stinnes, operating between North Europe, Mexico and the U.S. Gulf.

Finally, some operators called it a day. Hansa Heavy Lift, the successor to bankrupted Beluga Shipping, was the most prominent one. Hong Union Shipping of Shanghai just disappeared.

Q: Do you expect there to be a period of stability in the number of MPV operators, or are you expecting more insolvencies or mergers before the end of 2019?

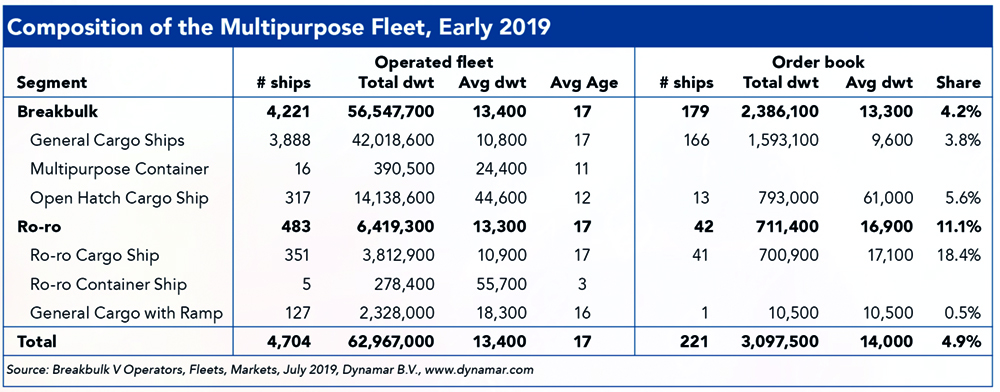

A: The current multipurpose orderbook, including open-hatch ships but excluding ro-ro, amounts to just 4.2 percent of the existing fleet. From 2009 to 2018, 1,577 vessels were built and 1,831 were scrapped, a clear sign of a shrinking fleet. Additionally, the 2020 IMO fuel sulfur regulation will no doubt induce additional scrapping.

We anticipate that as a result of this regulation the about 2,500 elderly ships built before 2000 will be scrapped more quickly. Hence, the overcapacity that has long plagued breakbulk carriers since the end of the 2005-2008 heydays has finally gone.

Instead of building ships, nowadays capacity requirement is increasingly sought in the pooling of ships and in incidental cooperation in the form of temporary joint services and the like.

Hence, we expect a period of stability in the number of breakbulk operators, rather than ongoing insolvencies or mergers.

However, what breakbulk operators cannot control is the activity of the disruptors, those being car carriers, container liners, reefer vessels and dry bulk carriers. The level of their competition depends on the demand for their core cargoes. When down, the interest in filling their ships with breakbulk cargoes amplifies, and vice versa.

Dynamar’s report provides an overview of important breakbulk and project shipping markets, sorted by major cargo segment, complemented by the main trade areas (destinations), with notes on developments, expectations, facts, findings, options and trends relevant to each cargo segment. The full publication, Breakbulk V (2019) – Operators, Fleets, Markets, is available from Dynamar at www.dynamar.com/publications/216.

Dirk Visser, senior shipping consultant and managing editor of Dynamar BV – Shipping Information and Consultancy, is a 30-year veteran of the liner shipping and forwarding industry in the Netherlands. Since 1999 he has been responsible for the publications and consultancy sections of Dynamar, including the DynaLiners portfolio of news and commentary, and Dynamar’s biennial flagship breakbulk publication.

Image credit: G2 Ocean